Murata Manufacturing Co. recently reported fourth-quarter earnings that surpassed analyst expectations, providing a clear window into the shifting priorities of the global electronics supply chain. As artificial intelligence infrastructure scales, the demand for high-performance passive components has surged, positioning traditional component manufacturers as unexpected beneficiaries of the generative AI boom. According to Bloomberg reporting, the company's ability to exceed market forecasts is directly tied to the expanding requirements of data center builders who are scrambling to integrate more sophisticated hardware to support large-scale language model training and inference.

This performance serves as a stark reminder that the AI revolution is not merely a software or processor-driven phenomenon, but a massive undertaking in physical engineering. While the market often fixates on GPU design and software capabilities, the underlying stability of these systems relies on thousands of minute, essential components. Murata’s success underscores a broader editorial thesis: the infrastructure layer of AI is creating a sustained, high-margin tailwind for legacy electronics firms that can adapt their manufacturing precision to meet the extreme demands of modern data centers.

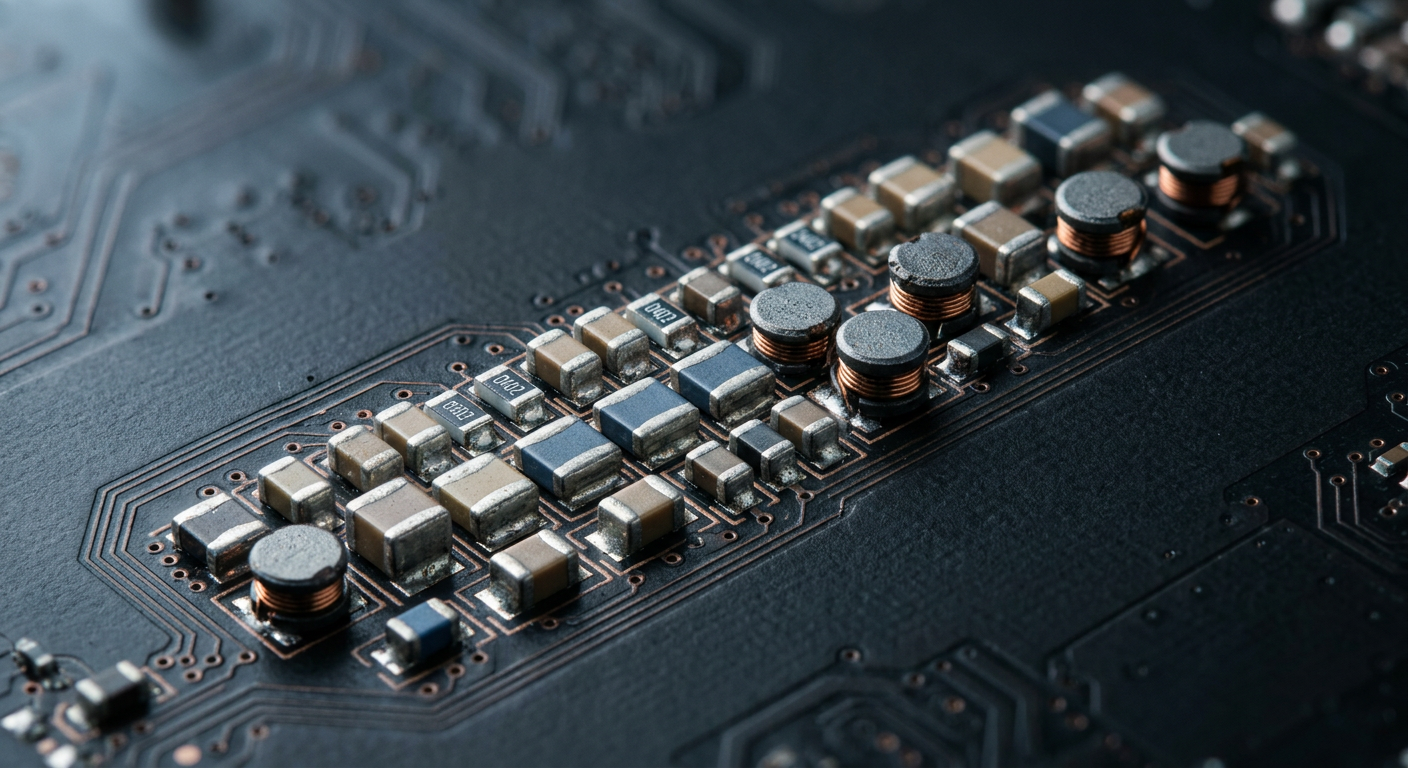

The Strategic Importance of Passive Components

Passive components—such as ceramic capacitors, inductors, and filters—are the unsung heroes of modern electronics. They manage voltage, filter noise, and ensure the steady flow of electricity in complex circuits. In the context of AI data centers, where power density has reached unprecedented levels, the role of these components has shifted from commodity-level utility to mission-critical infrastructure. High-performance computing chips, such as those produced by Nvidia or custom silicon from hyperscalers, require incredibly stable power delivery networks to function without error or thermal runaway.

As data centers transition to higher-wattage configurations, the failure of a single capacitor can lead to significant downtime or system instability. Murata, which maintains a dominant position in the global market for multilayer ceramic capacitors (MLCCs), has leveraged its manufacturing scale and precision to capture this high-end segment. The engineering challenge is not just about producing volume; it is about producing components that can withstand the intense heat and electrical stress inherent in racks filled with thousands of GPUs. This technical barrier to entry protects firms like Murata from lower-cost competition, allowing them to capture a premium for their specialized output.

Historically, component manufacturers were often viewed through the lens of cyclical consumer electronics demand. When smartphone or laptop sales slowed, these companies faced significant headwinds. However, the shift toward AI infrastructure provides a counter-cyclical buffer. Data centers operate on a different refresh cycle than consumer devices, and the sheer volume of components required for a single AI cluster dwarfs that of almost any other commercial application. This structural change in the demand mix is allowing firms to decouple their growth trajectories from the volatile consumer electronics market.

Mechanisms of the Infrastructure Supercycle

The mechanism driving this growth is the relentless push for power density in data centers. Modern AI servers are significantly more power-hungry than traditional web-hosting servers. This increased power demand requires more sophisticated power management integrated circuits (PMICs) and, by extension, more robust passive components to regulate the power path from the rack down to the individual silicon die. As these chips become more complex, the number of capacitors required per board has increased, effectively expanding the total addressable market for component suppliers even as the number of servers themselves grows.

Furthermore, the supply chain dynamics are shifting toward long-term partnership models. Hyperscalers—including Amazon, Google, and Microsoft—are now deeply involved in the design of their own server hardware. This has created a direct line of communication between component manufacturers and the end-users of the infrastructure. By working directly with these tech giants, suppliers like Murata can anticipate future hardware designs and optimize their production lines for specific performance characteristics. This integration reduces the uncertainty that typically plagues the electronics supply chain and allows for better inventory management, contributing to the improved profit margins observed in the latest earnings results.

This shift also reflects a broader trend of supply chain regionalization and risk mitigation. Data center operators are increasingly prioritizing reliability and supply chain security over the absolute lowest price. They are willing to pay a premium for components that are proven to be stable and available at scale. For a company like Murata, which has invested heavily in proprietary manufacturing processes and material science, this environment is ideal. It rewards the incumbent with technical superiority rather than punishing them for higher production costs.

Stakeholders and Market Tensions

For investors and industry analysts, the implications of this trend extend well beyond the balance sheet of a single manufacturer. The success of component suppliers acts as a leading indicator for the pace of data center expansion. If component supply becomes constrained, it creates a bottleneck that slows down the deployment of AI clusters across the globe. Regulators, meanwhile, are watching these supply chains closely, mindful of the potential for concentration risk in critical components. Should a few firms dominate the supply of essential capacitors, the geopolitical implications for data center independence could become a subject of future antitrust scrutiny.

Competitors are also forced to navigate this new reality. Smaller firms that cannot match the R&D spending required to innovate at the edge of power density may find themselves relegated to the lower-margin, legacy segments of the market. This creates a bifurcated industry landscape where the gap between high-end, AI-focused suppliers and general-purpose component manufacturers continues to widen. For consumers, the impact is indirect but significant: the sustainability of the current AI boom depends on the ability of this physical supply chain to keep pace with the software innovations that are driving the current wave of investment.

Uncertainties and the Path Forward

Despite the positive outlook, several questions remain regarding the long-term sustainability of this growth. One significant uncertainty is the potential for technological shifts that might reduce the reliance on traditional passive components. For instance, advancements in power delivery architecture or the development of integrated silicon-based capacitors could theoretically disrupt the current market model. Furthermore, should the pace of AI investment slow due to diminishing returns on model training, the demand for these specialized components would likely see a corresponding correction, testing the resilience of the current infrastructure build-out.

Another factor to watch is the capacity utilization of these manufacturers. While current demand is high, the industry has historically struggled with over-investment during peak cycles, leading to periods of supply gluts and price compression. Whether Murata and its peers can maintain disciplined capital expenditure while meeting the aggressive demands of hyperscalers will be a critical metric in the coming quarters. The market will also be looking to see if these companies can successfully transition their product mix toward the high-margin, AI-specific components without neglecting their core business areas, which remain vital for global revenue stability.

As the AI infrastructure build-out continues to evolve, the distinction between software-led growth and the physical reality of the hardware supporting it will become increasingly blurred. The question of whether this expansion can maintain its current velocity, or if it will face the inevitable bottlenecks of material science and manufacturing capacity, remains the central tension for the sector. As stakeholders continue to navigate the demands of high-performance computing, the role of foundational components will likely remain a key indicator of the broader health of the digital economy.

With reporting from Bloomberg

Source · Bloomberg — Technology