The global energy market remains caught in a state of precarious volatility. While a brief ceasefire agreement between Iran, the United States, and Israel initially pulled oil prices below $96 per barrel this week, the respite was short-lived. A subsequent strike on a Saudi Arabian pipeline underscored the fragility of the current landscape, reminding markets that geopolitical stability remains the primary variable in global supply chains.

Fatih Birol, executive director of the International Energy Agency (IEA), characterized the current moment as the most severe energy crisis in modern history. In an assessment that places the present disruption above the oil shocks of 1973, 1979, and the 2022 invasion of Ukraine combined, Birol noted that the world has never faced a supply interruption of this magnitude. The scale of the crisis is redrawing the map of energy security, forcing nations to reconcile immediate scarcity with long-term climate commitments.

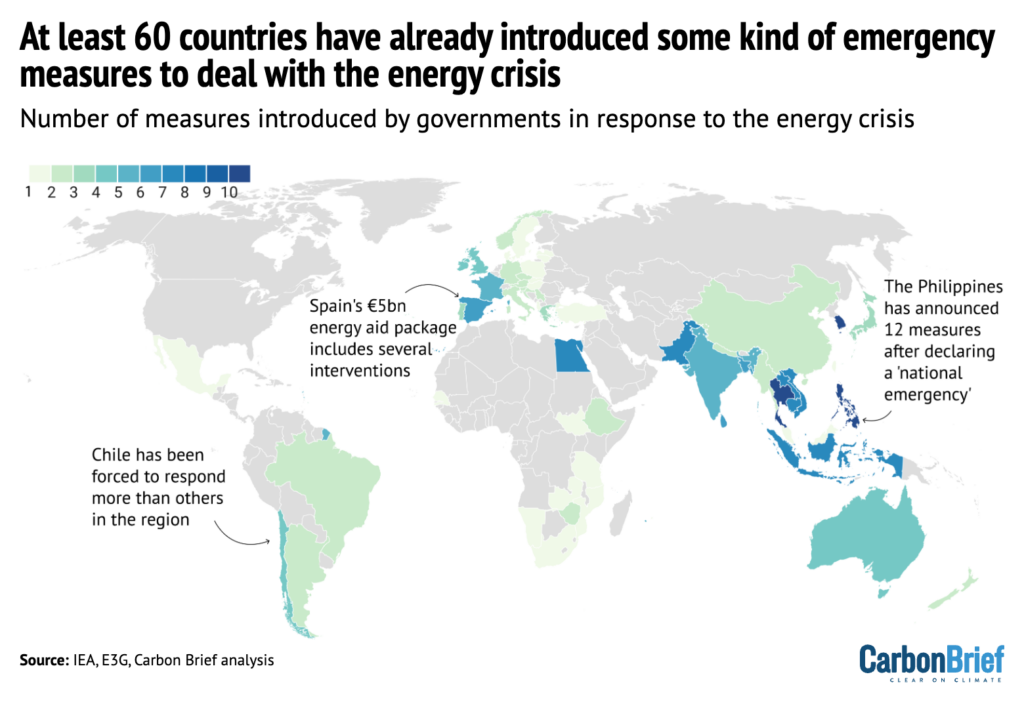

A crisis without precedent — and without a clean analogy

The comparison to the 1970s is instructive, but only up to a point. The 1973 Arab oil embargo and the 1979 Iranian Revolution each disrupted a single major source of supply in a world that was overwhelmingly dependent on crude oil for transport and industry. The global economy of the mid-2020s is structurally different: natural gas, coal, and electricity markets are now deeply interconnected across continents, meaning that a shock in one commodity ripples through the others with far greater speed and amplitude. When Birol describes the current crisis as exceeding those historical episodes, the claim rests not merely on the price of a barrel of oil but on the breadth of simultaneous disruptions across fuels and geographies.

The 2022 energy shock triggered by Russia's invasion of Ukraine offered a preview of this dynamic. European natural gas prices spiked to record levels, coal trade flows were rerouted, and electricity costs surged across dozens of countries. That episode, severe as it was, involved the partial curtailment of supply from a single major exporter. The current disruption appears to involve multiple points of failure in the Middle East — a region that still accounts for a dominant share of global crude exports and a significant portion of liquefied natural gas trade. The strike on Saudi infrastructure is a reminder that even the most heavily defended energy assets are not immune to the region's escalating tensions.

For importing nations — particularly in South and Southeast Asia, where energy demand continues to grow — the crisis poses an acute policy dilemma. Securing short-term supply often means signing long-term contracts for fossil fuels at elevated prices, locking in both cost and carbon exposure for decades. The alternative — accelerating deployment of domestic renewable capacity — addresses energy sovereignty but cannot replace dispatchable fossil generation overnight.

The paradox of windfall profits and accelerated transition

This instability has created a stark paradox: while fossil fuel producers are reaping historic profits from elevated prices, the very volatility of those markets is accelerating the transition to cleaner alternatives. High and unpredictable fuel costs strengthen the economic case for wind, solar, and battery storage, whose marginal cost of generation is essentially zero once installed. Every price spike makes the levelized cost comparison more favorable to renewables — and every pipeline attack makes the security argument harder to dismiss.

In the United Kingdom, the government faces increasing pressure over potential new drilling projects in the North Sea, which experts warn could undermine international climate targets. The tension is emblematic of a broader pattern: governments caught between the political imperative to lower energy bills today and the strategic imperative to decarbonize supply over the coming decades. Similar debates are playing out across Europe, where some member states have quietly extended the operational life of coal plants even as the bloc maintains its long-term emissions reduction framework.

The broader global trend, however, suggests that the current chaos is acting as a catalyst for diversification. The risks of fossil fuel dependency — price volatility, supply disruption, geopolitical leverage by exporting states — are becoming impossible to ignore at the sovereign level. Whether that recognition translates into durable policy or merely crisis-era rhetoric depends on choices that have not yet been made. The forces pulling in opposite directions — short-term scarcity demanding more extraction, long-term security demanding less dependence — remain unresolved, and the resolution will shape energy systems for a generation.

With reporting from Carbon Brief.

Source · Carbon Brief