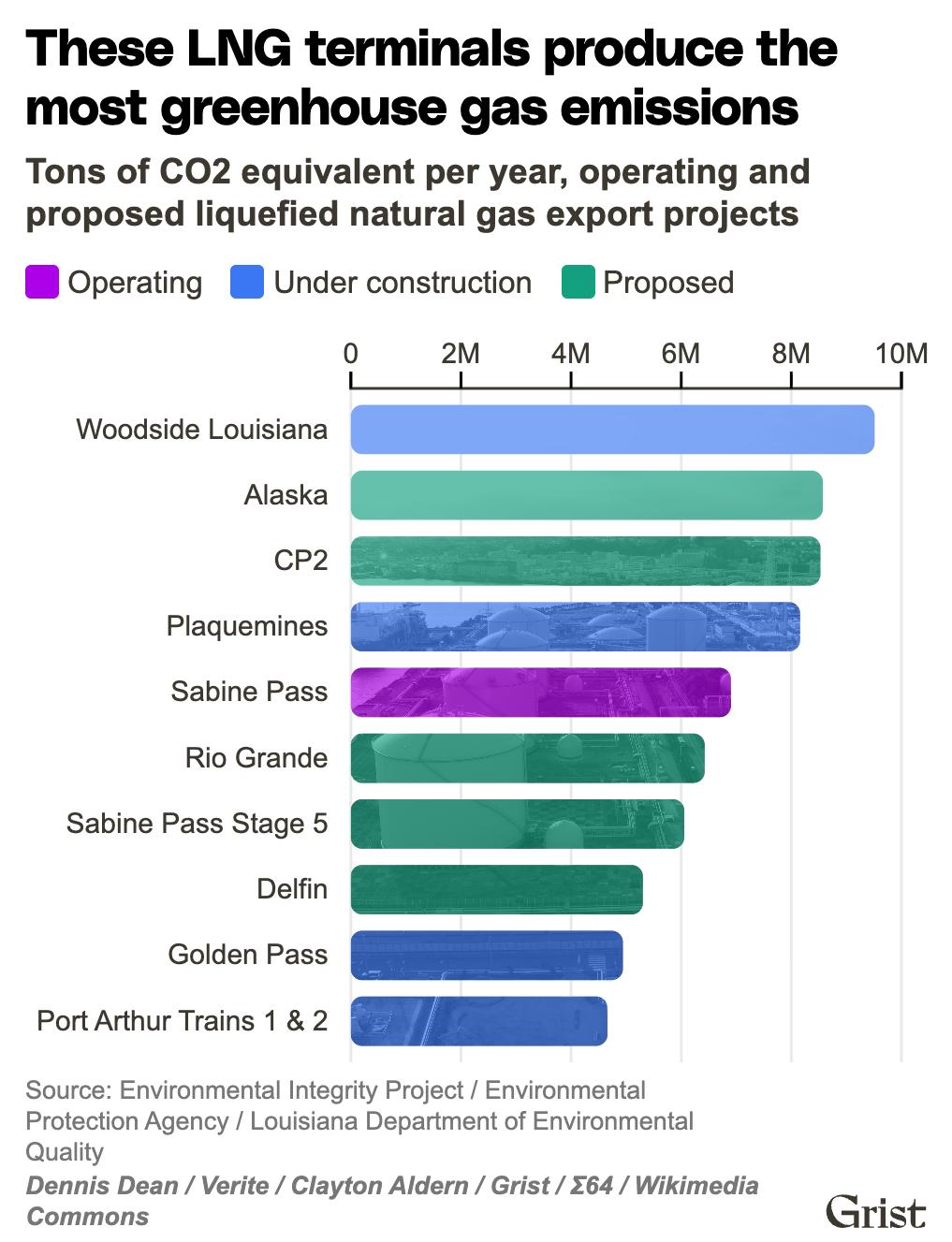

The narrative of Liquefied Natural Gas as a "bridge fuel" — a supposedly cleaner alternative to coal and oil — has long anchored Louisiana's industrial strategy. Since the state launched its LNG export boom in 2016, it has positioned itself as the epicenter of a global energy shift, channeling vast quantities of natural gas from domestic shale basins to overseas markets. But data from the state's existing infrastructure suggests the "cleaner" label is more marketing than reality. The Sabine Pass terminal, Louisiana's first major LNG export facility, already releases more greenhouse gases than the state's largest oil refineries.

Now, a new project is poised to dwarf those figures. In the marshlands near Lake Charles, Woodside Energy — Australia's largest oil and gas producer — is constructing a facility known as Louisiana LNG. At a reported cost of $18 billion, the terminal represents one of the largest foreign investments in the state's history. Yet, according to an analysis of federal and state records by Verite News, the project is on track to become the most carbon-intensive LNG facility in the United States, eclipsing every existing terminal and dozens of others proposed for the next decade.

The Bridge Fuel That Burns Both Ends

The concept of natural gas as a bridge fuel rests on a straightforward premise: when burned for electricity, gas produces roughly half the carbon dioxide of coal. That comparison, however, omits the full lifecycle of LNG — the energy-intensive process of cooling gas to minus 162 degrees Celsius for shipment, the methane that escapes during extraction and transport, and the emissions generated by the liquefaction infrastructure itself. Methane, the primary component of natural gas, is a far more potent greenhouse gas than carbon dioxide over shorter time horizons, meaning even modest leakage rates can erode or eliminate the climate advantage gas holds over coal.

Louisiana's Gulf Coast has become the proving ground for this tension. The state's existing LNG terminals already constitute a significant source of industrial emissions, and the sector's rapid expansion has outpaced the regulatory frameworks designed to monitor cumulative environmental impact. The addition of a facility projected to exceed all peers in carbon intensity raises a structural question about how emissions accounting is conducted in the permitting process — and whether the aggregate effect of multiple terminals along a single coastline receives adequate scrutiny.

The broader context is one of accelerating global LNG demand. European buyers, seeking alternatives to Russian pipeline gas since 2022, have turned to U.S. Gulf Coast terminals as a primary supply source. Asian markets, particularly in Southeast Asia, continue to expand gas import capacity as a complement to coal phase-down strategies. Louisiana sits at the intersection of these demand signals, and the economic incentives for the state — construction jobs, tax revenue, export earnings — are substantial. The political economy of LNG in Louisiana is not easily disentangled from the state's fiscal dependence on the energy sector.

Vulnerability Compounding Vulnerability

The expansion of heavy industrial infrastructure on the Gulf Coast arrives at a precarious moment. Louisiana is losing land to the sea at a rate that has reshaped its coastline within a single generation. Rising sea levels, subsidence, and the increasing intensity of Atlantic hurricanes place fixed industrial assets — pipelines, storage tanks, liquefaction trains — in a geography defined by escalating physical risk. The state has invested billions in coastal restoration, yet the forces driving land loss continue to accelerate.

For communities near Lake Charles, the calculus is immediate. The region has endured repeated hurricane strikes in recent years, and the concentration of petrochemical and LNG infrastructure means that extreme weather events carry compounding risks: facility damage, toxic releases, and prolonged economic disruption. Local advocates have pointed to the paradox of siting the nation's most emissions-intensive gas terminal in a region already bearing disproportionate costs from climate change.

The tension is structural, not incidental. Louisiana's role as a global energy hub generates revenue that funds public services and coastal protection, yet the emissions from that same hub contribute to the climatic forces eroding the coast. Whether the economic returns from facilities like Louisiana LNG can outpace the mounting costs of adaptation and disaster recovery is not a question the permitting process is designed to answer — but it is the question that will define the state's industrial future.

With reporting from Grist.

Source · Grist