The European battery landscape is undergoing a profound transformation, moving away from the singular ambition of domestic cell production toward the critical, often overlooked challenge of grid-scale energy storage. According to reporting from Breakit, Emad Zand, a former senior executive at the embattled battery manufacturer Northvolt, has secured 76 million Swedish kronor in equity capital for his new venture, Tavion. The company, which has also reportedly secured half a billion kronor in debt financing, aims to deploy battery parks across the continent to manage the intermittent nature of renewable energy sources.

This capital injection arrives at a pivotal moment for the European green transition. While the collapse of Northvolt served as a sobering reminder of the extreme capital intensity and execution risks inherent in gigafactory operations, Zand’s pivot suggests a strategic recalibration. By focusing on the deployment of battery infrastructure rather than the manufacturing of cells themselves, Tavion is positioning itself within a different segment of the energy value chain—one that is arguably more essential to the immediate stability of the European power grid as it integrates higher volumes of wind and solar capacity.

The Strategic Pivot from Manufacturing to Infrastructure

The ambition to build a domestic battery manufacturing base in Europe was, for years, predicated on the necessity of regionalizing supply chains to compete with Asian and North American incumbents. However, the operational difficulties faced by firms like Northvolt revealed the fragility of this model when confronted with volatile commodity prices, complex supply chain logistics, and the sheer scale of investment required to achieve competitive unit economics. The market is now witnessing a structural shift where capital is flowing toward the downstream application of battery technology.

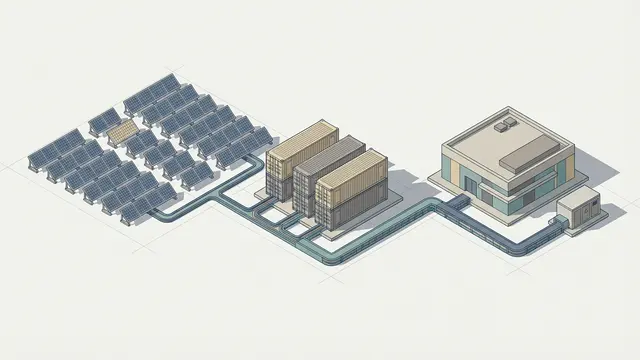

Battery parks, or utility-scale storage systems, act as the shock absorbers of the modern grid. As Europe accelerates its decarbonization efforts, the penetration of variable renewable energy (VRE) has created significant technical challenges for grid operators. Unlike traditional baseload power plants, wind and solar farms cannot be dispatched on demand. This creates a structural need for large-scale storage that can discharge energy during periods of peak demand or low generation. Tavion’s business model essentially bets on the arbitrage potential of these systems and the increasing necessity for frequency regulation services.

This shift is not merely a change in product focus; it is a change in risk profile. Manufacturing cells requires massive capital expenditure (CapEx) in specialized machinery and faces the constant threat of technological obsolescence from newer chemistries or more efficient production methods. Conversely, the development of battery parks is primarily a project finance exercise. It involves navigating land-use regulations, grid interconnection queues, and power purchase agreements. While these projects are not without their own regulatory and bureaucratic hurdles, they are largely shielded from the manufacturing-specific risks that have recently plagued the European industrial sector.

The Economics of Grid-Scale Storage

To understand why investors are backing ventures like Tavion, one must look at the mechanics of the European electricity market. The volatility of energy prices has increased significantly over the last few years, driven by geopolitical instability and the transition to renewables. For a battery park operator, this volatility is a feature, not a bug. By purchasing electricity when supply exceeds demand—often at negative prices—and selling it back to the grid when demand spikes, these facilities can capture significant margins.

Furthermore, European transmission system operators (TSOs) are increasingly looking to third-party providers to help maintain grid frequency. As conventional thermal power plants, which traditionally provided the inertia required to stabilize the grid, are retired, battery parks are stepping in to provide synthetic inertia and fast-frequency response services. These ancillary services provide a predictable, long-term revenue stream that complements the more speculative arbitrage revenue. This dual-revenue model is the bedrock upon which the financial viability of such infrastructure projects is built.

However, the success of this model is heavily dependent on the regulatory environment. Each European nation has its own distinct market structure, grid connection standards, and subsidy schemes. A pan-European strategy, which Zand appears to be pursuing, requires a high degree of operational agility to navigate these fragmented regulatory landscapes. The ability to scale across borders will likely determine which firms emerge as winners in the energy storage race, as the cost of capital remains highly sensitive to the perceived risks of individual market regulations and grid infrastructure readiness.

Stakeholders and the Changing Energy Landscape

For regulators and policymakers, the rise of battery parks represents a shift in the definition of energy security. While the initial focus was on "battery sovereignty"—the ability to produce the physical components domestically—the current priority is grid resilience. Regulators are now under pressure to streamline the permitting processes for these storage facilities. The bottleneck is no longer just the availability of batteries, but the capacity of the grid to absorb them and the speed at which developers can secure interconnection agreements.

Competitors in this space are not just other startups, but also established utilities and independent power producers (IPPs) that are increasingly integrating storage into their existing portfolios. These incumbents have the advantage of existing grid connections and deep balance sheets, but they often struggle with the agility required to deploy modular, software-driven storage solutions at speed. This creates a space for specialized players like Tavion, which can focus exclusively on the optimization and deployment of these assets without the legacy baggage of traditional utility operations.

For consumers, the proliferation of these parks is a necessary, if invisible, component of a lower-carbon future. While they do not directly lower energy prices in the short term, they are critical to preventing the grid instability that could otherwise necessitate more expensive, carbon-intensive backup generation. The long-term success of the energy transition relies on these storage assets to smooth the transition, making them a central pillar of European energy policy in the coming decade.

Open Questions and the Outlook for Storage

Despite the clear market demand for grid-scale storage, several uncertainties remain. The rapid pace of technological development, particularly in battery chemistries beyond traditional lithium-ion, could alter the economics of these parks. If long-duration energy storage (LDES) technologies, such as flow batteries or thermal storage, reach commercial maturity, the current generation of lithium-ion parks may face competitive pressure. Developers must build their infrastructure with enough flexibility to accommodate these future shifts in technology.

Furthermore, the long-term sustainability of the supply chain for the batteries themselves remains a global concern. Even if the cells are not manufactured in Europe, the sourcing of critical minerals and the environmental impact of battery production continue to attract intense scrutiny. As the sector matures, developers will likely be held to higher standards regarding the carbon footprint of their supply chains and the recyclability of their assets at the end of their lifecycle. The interplay between these environmental mandates and the need for rapid deployment will continue to define the operational challenges for firms like Tavion.

As the European energy sector continues to move toward a decentralized and intermittent power architecture, the role of storage developers will become increasingly central to the continent’s economic stability. Whether these new ventures can successfully navigate the complexities of cross-border infrastructure development while managing the inherent risks of the energy market remains an open question for the coming years. The transition is underway, but the final configuration of Europe’s grid remains a work in progress.

With reporting from Breakit

Source · Breakit