Spanish renewable energy producer Solaria Energía y Medio Ambiente SA has successfully raised approximately €300 million through a share offering, signaling a strategic shift in how energy firms approach the burgeoning demand from the digital economy. According to Bloomberg reporting, the company intends to deploy these funds to bolster its capabilities in data center infrastructure and battery storage systems, marking a deliberate move to capitalize on the energy-intensive nature of modern computing.

This capital infusion arrives at a pivotal moment for European energy markets, where the intersection of decarbonization goals and the explosive growth of artificial intelligence has created a unique bottleneck. By aligning its asset base with the needs of large-scale data facilities, Solaria is positioning itself not merely as a power generator, but as a critical infrastructure partner for the digital age. This development serves as a case study for how traditional utility players are reconfiguring their business models to address the specific power density challenges posed by modern data architectures.

The Convergence of Infrastructure Assets

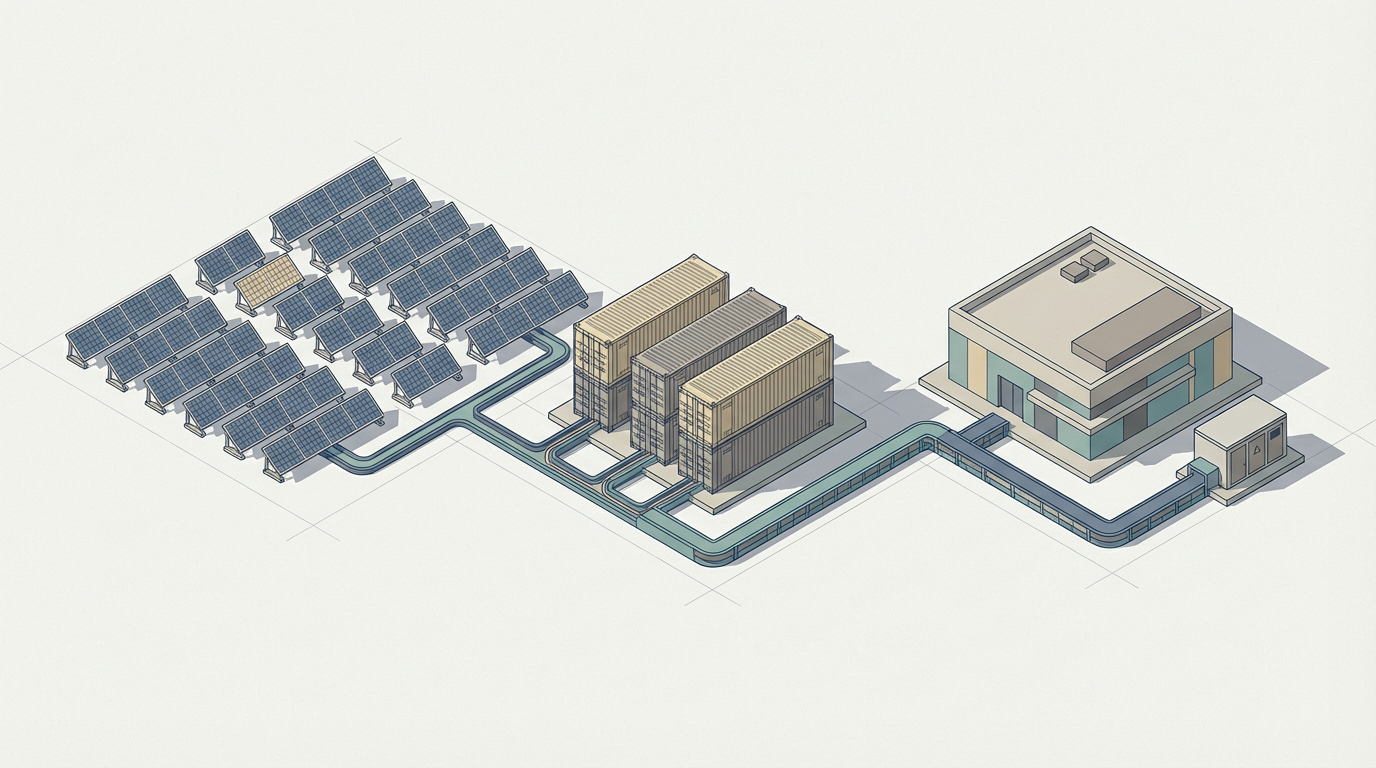

The traditional model of renewable energy production—selling electricity into a wholesale grid—is increasingly being supplemented by more direct, integrated partnerships with high-demand consumers. Data centers, which require constant, high-quality power, represent a departure from the intermittent nature of wind and solar energy. By investing in battery storage, Solaria is effectively creating a buffer that allows them to offer the baseload-like reliability that hyperscalers and data center operators demand. This transition reflects a broader structural shift in the energy sector, where the value proposition is moving from simple generation to the provision of reliable, managed energy services.

Historically, the energy sector and the technology sector operated in distinct silos, with utilities serving as passive providers and tech firms acting as retail consumers. The current environment, characterized by the massive power requirements of large language models and global cloud infrastructure, has rendered this separation obsolete. Companies like Solaria are recognizing that their competitive advantage lies in their ability to bridge the gap between renewable generation and the specific needs of the digital economy. This is not merely a diversification strategy; it is a fundamental reorientation toward the infrastructure that will define the next decade of industrial growth.

Mechanisms of the Energy-Compute Nexus

The economic logic behind this move is driven by the specific operational incentives of the data center industry. Hyperscalers are under immense pressure to meet sustainability targets while simultaneously scaling their compute capacity, which requires an unprecedented amount of electricity. By securing capital for both renewable generation and the storage solutions necessary to manage that energy, Solaria is mitigating the risk of grid volatility. The deployment of battery systems acts as a critical mechanism for load balancing, ensuring that data centers can maintain operations even when renewable output fluctuates due to environmental variables.

Furthermore, the capital structure of this investment highlights the confidence of the financial markets in the long-term viability of the energy-compute nexus. Investing in the physical infrastructure that supports data centers offers a degree of stability that pure-play renewable energy projects might lack in a saturated market. By integrating battery storage, the company is also capturing value throughout the supply chain, from the generation of clean electrons to the stabilization of those electrons for high-performance computing loads. This dual-pronged approach allows the firm to command higher margins by offering a more robust, integrated energy product rather than a commodity-like service.

Stakeholder Implications and Market Dynamics

For regulators and policymakers, the emergence of energy-integrated data infrastructure presents both a challenge and an opportunity. On one hand, the concentration of power-intensive facilities in specific regions can place significant strain on existing electrical grids, necessitating rapid upgrades and localized energy solutions. On the other hand, the private investment channeled into these projects—such as Solaria’s latest raise—lessens the burden on public infrastructure by fostering self-sustaining energy ecosystems. Regulators must now balance the need for grid stability with the imperative to support the digital infrastructure that underpins modern economic competitiveness.

Competitors in the renewable space will likely observe these movements closely, as the pressure to differentiate in a market increasingly focused on reliable, high-quality power delivery intensifies. For the consumer, the impact is indirect but significant; the success of such models could lead to a more resilient digital landscape, though it also raises questions about the allocation of energy resources. As large-scale energy producers become more deeply embedded in the tech stack, the traditional boundaries of the utility sector will continue to blur, necessitating new frameworks for oversight and market participation that reflect the reality of this integrated landscape.

Outlook for Integrated Energy Systems

The long-term implications of this pivot remain subject to several variables, most notably the speed at which battery technology can scale to meet the massive requirements of data centers. While the current investment provides a strong foundation, the transition toward fully integrated, renewable-powered computing will require continuous innovation in storage efficiency and grid management software. The ability of companies like Solaria to successfully execute on these projects will be a key indicator of whether the model can be replicated at the scale required by the global tech industry.

Observers should monitor how these firms navigate the regulatory hurdles associated with developing both energy generation and digital infrastructure. As the demand for computing power continues to climb, the tension between grid capacity and energy consumption will likely persist, potentially leading to further consolidation or strategic partnerships between energy producers and technology providers. The question remains whether this model will become the industry standard for energy-intensive digital infrastructure or remain a niche strategy for early movers in the renewable space.

As the intersection of energy generation and high-performance computing matures, the strategic importance of firm-level infrastructure investments will only grow. The success of this capital deployment will likely serve as a bellwether for how the European energy market adapts to the requirements of the digital era, revealing whether existing firms can successfully pivot to meet the demands of a new, power-hungry industrial paradigm.

With reporting from Bloomberg

Source · Bloomberg — Technology